July 24, 2026

Key Insights

- SpaceX is setting the stage to issue one of the largest ever initial public offerings.

- It could set the stage for a number of other large private companies to do the same in 2026.

- The SpaceX valuation is predicated on not just launch services, but a suite of integrated services positioned to be profitable well into the future.

- If SpaceX’s Starship project proves to be successful, it could be a game changer in launch economics.

- SpaceX is uniquely positioned, even in the broader launch and aerospace industries.

Latest from EdgeRock

Questions? Talk to our team.

Find out how truly custom, independent planning can impact your portfolio.

Start a Conversation

SpaceX is going public. Are we about to witness a generational market event?

By Rob Foss

June 1, 2026 |

By Rob Foss

The Elon Musk-led SpaceX is about to issue the largest public offering in market history. Here's why everyone should be paying attention.

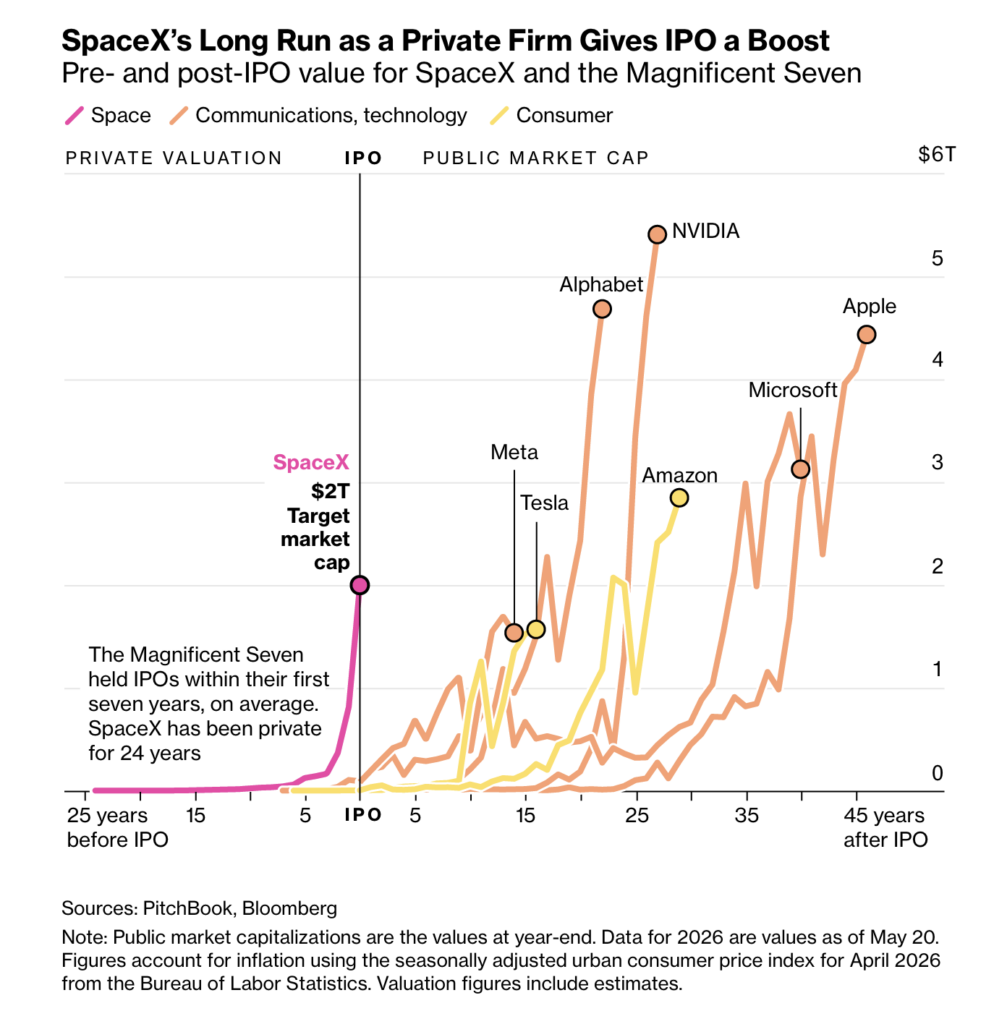

SpaceX filed its S-1 with the SEC last week, setting the stage for a listing on the NASDAQ later this year. The reported terms: a capital raise of roughly $75 billion at a valuation between $1.5 trillion and $1.75 trillion.

If it prices anywhere near that range, it will be the largest public offering in history—nearly three times the size of Saudi Aramco’s record-setting $25.6 billion debut in 2019. A transaction of that scale doesn’t read like an IPO. It reads like a sovereign-scale liquidity event. On day one of trading, SpaceX would slot in among the most valuable companies on earth, ahead of every major industrial firm and behind only the very largest mega-cap technology platforms.

What makes this listing genuinely different from the mega-deals it would dethrone isn’t the size. It’s that the company underneath the deal is doing something structurally new. Aramco was the world’s largest oil producer going public. Alibaba was the largest e-commerce platform in the largest consumer market. Both were already well understood. SpaceX, by contrast, is bringing four interlocking businesses to market—launch, broadband, defense, and AI infrastructure—each of which is reshaping its industry, and all of which run on a shared technology stack that no competitor has matched.

A founder on the cusp of becoming a paper trillionaire

Elon Musk founded SpaceX in 2002 with a personal check large enough to keep the lights on but small enough that the first three Falcon 1 launches all failed before the fourth one made orbit. He also runs Tesla, already one of the most valuable industrial companies in the world.

If SpaceX prices near the top of its rumored band, Musk could become the first paper trillionaire in history. For perspective, John D. Rockefeller—the previous benchmark for individual American wealth—was estimated at roughly $1.4 billion at his 1916 peak, which adjusts to somewhere north of $400 billion in today’s dollars. A trillion is a different category. It is larger than the annual GDP of Switzerland, the Netherlands, or Saudi Arabia.

That number says less about any single founder than it does about the structural concentration of value in a handful of AI-and-aerospace ecosystems. The unprecedented wealth being created across artificial intelligence, aerospace, energy, robotics, and communications is showing up in a small number of balance sheets, and Musk happens to control the largest stake in several of them.

A rocket company that isn’t really a rocket company

The bigger story is what SpaceX actually sells. Launch services are the headline. The cash flow is somewhere else.

Starlink, the satellite broadband business, now provides coverage in roughly 150 countries and territories. Subscriber count has reached 10 million, up from 2 million in 2023. The customer mix is wider than most investors realize: rural Americans who never had broadband, ocean shipping companies, RV travelers, in-flight Wi-Fi on multiple major airlines, militaries fighting in Ukraine and elsewhere, and a fast-growing list of enterprise customers who need connectivity in places terrestrial fiber will never reach economically.

By the numbers, Starlink reportedly generated approximately $11.4 billion of SpaceX’s estimated $18.6 billion in 2025 revenue. (Translation: SpaceX is, by cash flow, a connectivity company that happens to own the world’s best launch system.)

The analogy that fits best is Amazon. For its first decade, Amazon was an online bookstore that happened to be building world-class logistics and computing infrastructure. By the time anyone noticed, the bookstore was a rounding error and AWS was generating most of the operating income. Starlink is having that same kind of moment inside SpaceX. The launch business made the company famous. The connectivity business is what makes the valuation make sense.

Why launch economics are the real story

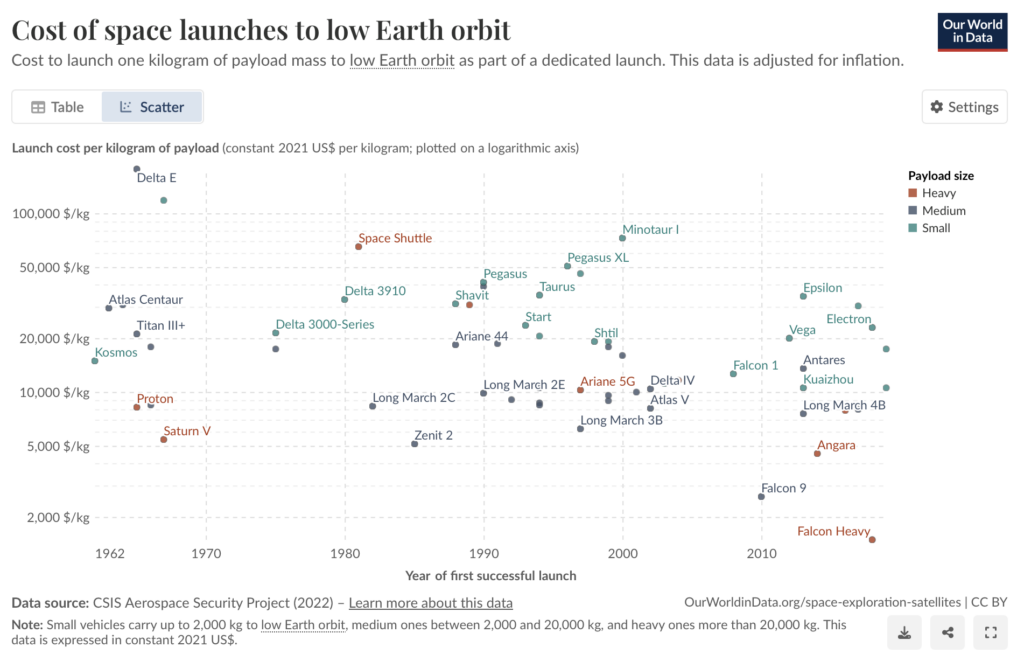

That cash flow funds the next leg—Starship. The Falcon platform already delivers payloads to low Earth orbit at roughly $7,000 per kilogram. If Starship achieves full reusability at scale, that cost could fall below $200 per kilogram.

This is the most important number in the entire S-1 story.

For context, the Space Shuttle’s all-in cost was around $54,000 per kilogram. That meant for nearly half a century, the only customers who could afford to put real mass in orbit were governments, defense agencies, and a small number of telecom operators. Space was a niche premium business, the way air travel was in 1955.

A move from $7,000 to $200 per kilogram is the orbital equivalent of containerization. Marc Levinson’s history of the shipping container makes the point well: the box itself was a simple piece of steel. What it did was collapse shipping costs by roughly 90 percent and, in doing so, made globalization economically viable. Entire industries that didn’t exist beforehand—just-in-time manufacturing, the trans-Pacific consumer electronics supply chain, the modern auto industry—organized themselves around the new cost curve.

A 97 percent drop in launch costs would do something similar. Large-scale orbital infrastructure, in-space logistics, satellite servicing, manufacturing in microgravity, deep-space industrial activity, and cislunar commerce all stop being PowerPoint slides and start penciling out as real businesses. None of those industries exists at scale today, not because the technology is missing but because nobody could afford to get the mass up there. SpaceX is betting that it can solve the cost problem and let the rest follow.

The xAI integration changes the equation

Earlier this year, Musk pulled his artificial intelligence company, xAI, into closer orbit with SpaceX-related initiatives. xAI also controls X, formerly known as Twitter, which gives it a real-time data firehose few competitors can match.

The strategic logic is straightforward. Starlink generates the data and the bandwidth. xAI builds the models. The satellite network becomes a globally distributed communications and compute backbone.

Musk has openly floated the idea of orbital data centers powered by near-constant solar energy. That isn’t science fiction posturing. It’s an attempt to route around what has become the single biggest bottleneck on the AI buildout: power and cooling. NVIDIA can produce all the GPUs the market wants, but the grid in northern Virginia, central Ohio, and the data center corridors of Texas and Arizona is running into physical limits. Utilities are quoting three-to-seven-year interconnection queues for new hyperscale facilities. Orbital compute sidesteps those constraints entirely—solar power is constant in low Earth orbit, and the vacuum makes cooling easier rather than harder.

Even short of orbital data centers, the more immediate payoff is autonomous network management. Embed Grok-class models directly into Starlink and the network gains the ability to optimize routing, anticipate congestion, allocate bandwidth, and reduce latency in real time. The result is a vertically integrated stack spanning launch, satellites, communications, AI, and (plausibly) orbital compute itself.

A platform that’s almost impossible to replicate

Each piece makes the others more valuable. Starlink funds launch innovation. Cheaper launch makes more satellites economic. Smarter networks make those satellites more useful. The whole stack anchors an AI buildout that no competitor can match. It is the same flywheel logic that made Amazon, Google, and Apple impossible to dislodge once they reached scale—each business reinforces the next, and the cost of building the entire stack from scratch becomes prohibitive.

Amazon Kuiper, the only Western competitor at similar scale, is still trying to get a fraction of the satellites Starlink has already deployed. China’s state-backed constellation programs are technically capable but operate under export and political constraints that limit their global reach. The European IRIS² constellation is years from operational scale and faces ongoing political wrangling among member states.

That competitive moat is the most charitable explanation for the valuation. It is also the source of the risk, because the price already assumes the flywheel keeps spinning despite ongoing concerns about profitability and capital intensity. Investors are not buying current cash flows. They are buying a future in which all four legs of the stack continue to extend their leads simultaneously.

A quasi-industrial-policy company

SpaceX is now embedded deep in U.S. national security infrastructure—launch contracts, military communications, defense applications, intelligence community satellites, and emerging hypersonic test platforms. Launch reliability, deployment cadence, and secure communications are no longer just commercial capabilities. They are strategic geopolitical assets.

The closest historical parallel is Boeing in the second half of the twentieth century. Boeing was nominally a commercial aircraft manufacturer, but its position in U.S. defense procurement, the strategic missile program, and NASA contracting made it inseparable from American industrial policy. Decisions made in Seattle were, in real terms, decisions about U.S. strategic capability.

SpaceX is on a similar trajectory. The U.S. defense industrial base has been contracting for three decades, with a handful of prime contractors absorbing most of the work. SpaceX represents the first genuine new entrant at scale in a generation. In practice, the company is evolving from an aerospace business into something closer to an industrial-policy platform aligned with long-term U.S. aerospace, communications, and defense priorities.

Why this matters beyond the size of the deal

A successful SpaceX listing could meaningfully reopen the late-stage technology IPO market, which has been largely frozen since the post-2021 tightening cycle. OpenAI and Anthropic have both signaled eventual public listings. A clean SpaceX print could pull forward IPO timelines for Stripe, Databricks, and others in that cohort.

Scale also matters for benchmarks. Once SpaceX is included in major equity indices, passive funds and institutional mandates become forced buyers—a structural tailwind that tends to reinforce liquidity and valuation in the early innings of public trading. A position this size cannot be ignored by any institutional portfolio that benchmarks to the major indices.

The deeper structural point is the one EdgeRock has been making for years: the U.S. public market is shrinking. In 1996, roughly 8,000 domestic companies were listed on U.S. exchanges. Today, that number is closer to 4,500.¹¹ The reasons are well documented—Sarbanes-Oxley raised the cost of being public, the JOBS Act made staying private easier, and the explosion of private capital meant late-stage companies could raise multi-billion-dollar rounds without ever bothering with the public markets.

The consequence is that ordinary investors have been quietly locked out of the highest-growth phase of the most important companies of the last twenty years. Facebook went public after most of its growth was in the past. So did Uber. Stripe and Databricks have stayed private for over a decade, raising tens of billions in private rounds while ordinary 401(k) holders watched from the sidelines. Reopening the IPO market would not undo that shift overnight, but it would be unambiguously good for public investors: deeper opportunity sets, better capital formation, and—if the door stays open—a path for smaller and mid-sized companies to come public earlier rather than staying private indefinitely.

The risks are real

None of this is free. SpaceX operates in one of the most capital-intensive industries on earth, with significant execution, regulatory, geopolitical, and technological risk. Starship’s economics are unproven at scale, and every prior step-change in launch cost has taken longer than its proponents promised.

The valuation already discounts simultaneous success across launch, broadband, defense, and AI infrastructure. Any one of those legs underperforming materially would force a meaningful re-rating. The long-duration nature of the cash flows leaves them unusually exposed to interest rates, capital availability, and investor appetite for long-dated growth assets—the same risk profile that punished similar names through 2022.

There is also concentrated key-person risk. Musk runs Tesla, xAI, and SpaceX simultaneously, and his attention is finite. Regulatory risk is non-trivial: Starlink relies on spectrum allocations that governments can revoke, and Starship’s environmental review process has already slipped multiple times. And the historical track record of the largest IPOs in history is sobering—of the five biggest before SpaceX, only Visa has meaningfully outperformed the market, and Aramco has lost value.

Investor enthusiasm is warranted. So is investor humility.

The bigger picture

Strip away the deal mechanics and what’s left is a signal. If the offering prices and trades well, it cements the new capital expenditure cycle—AI, energy, aerospace, communications, advanced manufacturing—as the dominant equity story for the rest of the decade.

These sectors are no longer running on separate tracks. The same companies are building the data centers, the satellites, the launch systems, the models, the energy infrastructure, and the manufacturing capacity, often through overlapping ownership and shared technology platforms. The capex super-cycles of past eras—railroads in the 1880s, electrification in the 1920s, the fiber buildout of the 1990s—each defined a generation of equity returns. The current cycle has the same fingerprints, and SpaceX is the clearest expression of it yet.

For a generation of investors who grew up watching the public markets shrink, this is the most consequential listing in years. It is also the clearest evidence to date that the next great capex cycle is no longer ahead of us. It is happening now.

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal, tax, or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, and EdgeRock Wealth Management, LLC makes no representation or warranty as to the accuracy or completeness of the information, which should not be used as the basis of any investment decision. Information contained on third party websites that EdgeRock Wealth Management, LLC may link to is not reviewed in their entirety for accuracy and EdgeRock Wealth Management, LLC assumes no liability for the information contained on these websites. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of writing and are subject to change without notice. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from EdgeRock Wealth Management, LLC.

Related Posts

About the Author

Related Posts

Don’t fear the Buffett indicator

April 3, 2024Why investors shouldn’t hide from market corrections

April 7, 2025

Read more Insights