April 6, 2026

Key Insights

- Not all Roth IRA strategies are equal and require careful planning.

- Even though Roth contributions have limitations, there are often overlooked opportunities.

- Roth conversion strategy is year-round, not just an end-of-year checkbox.

Latest from EdgeRock

Questions? Talk to our team.

Find out how truly custom, independent planning can impact your portfolio.

Start a Conversation

Understanding Roth Contributions vs. Roth Conversions

By Ryan Murphy

November 25, 2024 |

By Ryan Murphy

Roth IRAs can be an powerful tool in any retirement strategy. But the rules for funding them aren't always obvious. Let's talk about the difference between Roth contributions and Roth conversions.

When planning for retirement, Roth accounts often emerge as a powerful tool. They offer tax-free growth and tax-free withdrawals in retirement. However, not all Roth strategies are created equal. Let’s dive into the key differences between Roth Contributions and Roth Conversions, and when each strategy might fit into your financial plan.

Roth Contributions

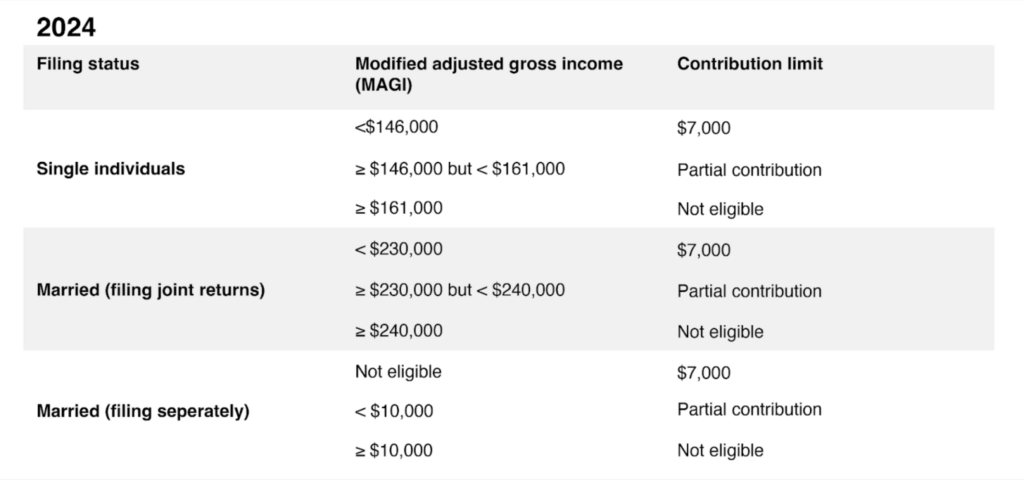

A Roth contribution is a powerful tool for retirement savings, allowing you to invest after-tax dollars and potentially withdraw your earnings tax-free in retirement. To make a Roth contribution, you must have earned income, such as wages, salary, or self-employment income. There are income limits for Roth IRA contributions, which vary based on your filing status.

For single filers in 2024, the phase-out range for Roth IRA contributions is between $146,000 and $161,000. This means that if your modified adjusted gross income (MAGI) is below $146,000, you can contribute the full $7,000 ($8,000 if age 50 or older). If your MAGI is above $161,000, you cannot contribute to a Roth IRA. For married couples filing jointly, the phase-out begins at $230,000 and ends at $240,000.

Eligibility & Limits

Employment Income Required: You must have earned income (e.g., wages, salary, or self-employment income) to make a Roth IRA contribution. If you’re married, your spouse’s income can count if you file jointly.

Contribution Limits: For 2024, you can contribute up to $7,000 annually ($8,000 if age 50 or older) to a Roth IRA, subject to income phase-out limits:

Single Filers: Phase-out begins at $146,000; ineligible at $161,000.

Married Filing Jointly: Phase-out begins at $230,000; ineligible at $240,000.

Roth 401(k): No income limits, but total employee deferrals (across traditional and Roth 401(k)) cannot exceed $23,00 ($30,500 if age 50+).

Where do contributions come from?

Earned Income: Must match or exceed your contribution.

Savings or Investment Accounts: While you must have earned income, the actual dollars contributed can come from savings or other non-retirement investment accounts.

Roth Conversions

A Roth conversion involves moving funds from a traditional IRA or 401(k) to a Roth IRA. Unlike Roth contributions, Roth conversions have no income limits, meaning anyone can perform a conversion regardless of their income level. However, it’s important to note that a Roth conversion is a taxable event, meaning you’ll owe income tax on the amount you convert in the year of the conversion. The funds you convert must come from a pre-tax retirement account, such as a traditional IRA or 401(k), or from non-deductible IRA contributions.

Key Features

No Income Limit: Unlike contributions, anyone can do a Roth conversion, regardless of income.

Taxable Event: The amount converted is added to your taxable income for the year. For example, if you convert $20,000, you’ll pay income taxes on that $20,000 at your marginal tax rate.

No Earned Income Requirement: You can perform a conversion even if you have no earned income for the year.

Where do conversion funds come from?

Traditional IRA or 401(k): Funds must be in a pre-tax account.

Non-Deductible IRA Contributions: Can be converted tax-efficiently, especially if you have no other pre-tax IRA balances (this avoids the pro-rata rule).

When to consider a Roth conversion

Low-Income Year: When you’re in a lower tax bracket, converting minimizes the tax hit.

Before RMDs Start: Conversions can help reduce future required minimum distributions (RMDs) from traditional accounts.

Tax Diversification: Having tax-free income in retirement offers flexibility to manage taxes strategically.

Which strategy is right for you?

You may want to consider a Roth conversion if you’re in a low-income year to minimize the tax impact, if you want to reduce future Required Minimum Distributions (RMDs) from traditional accounts, or if you want to diversify your retirement income sources by having both taxable and tax-free income.

Ultimately, the decision between a Roth contribution and a Roth conversion is a personal one. While both strategies offer tax advantages, they have distinct implications for your financial future. Consider your current tax bracket, anticipated future income, and long-term goals when making your choice. A Roth contribution can provide tax-free growth and withdrawals in retirement, while a Roth conversion offers immediate tax benefits and potential flexibility. To make the best decision for your specific circumstances, consulting with a qualified financial advisor is highly recommended.

Related Posts

Turning market volatility into a tax opportunity

March 25, 2026Digging beneath the surface of the market

May 6, 20252025 mid-year market update

June 4, 2025

About the Author

As Director of Marketing, Ryan helps introduce EdgeRock to Colorado families and business owners. In a previous life, he reported on sports and culture for SBNation and The Denver Post.

Related Posts

Questions to ask when you meet a financial advisor

September 9, 2025Turning market volatility into a tax opportunity

March 25, 2026

Read more Insights